PHOTO COURTESY OF ART BASEL

Share this article:

A STRANGE BALANCE OF THE 2025 ART MARKET; MORE ART LESS MONEY!

The latest Art Basel& UBS Global Art Market Report 2026, written by economist Clare McAndrew, describes a year in which art market did something unusual; it shrank in value but expanded in activity. This paradox was the most surprising thing about last year’s art market, in other words, the market became smaller, but more active the same time.

According to the report, global art sales fell to about $57.7 billion, a drop of around 12%. Yet the number or art works sold actually increased, reaching more than 40 million transactions.

In simple terms: in 2025 more art circulated, but at lower prices.

For many art market observers, this is the most important structural change in the market.

THE END OF THE “TROPHY ART” MOMENT

For several years the art world was obsessed with spectacular auction records: paintings selling for $50 million, $100 million, even more.

Last year according to the Art Basel & UBS Global Art Market Report, that part of the market suddenly cooled. The number of artworks selling for more than $10 million dropped by about 39%.

This is significant because the global art market is usually driven by a tiny number of ultra- expensive works. When those record sales disappear, the total market value quickly falls.

So I may call simply, the headline of the year was fewer billionaire purchases.

A MARKET BECAME MORE “DEMOCRATIC”

But, according to the report, something else happened at the same time.

The lower and mid-price segments became more active. Galleries reported stronger sales of works priced under a few thousand dollars, and many collectors bought smaller pieces rather than major masterpieces.

From a cultural perspective this is quite interesting.

Instead of being dominated by a few spectacular masterpieces, the market looked more like a broad ecosystem of smaller transactions.

I could read that as the art market became less theatrical and more every day.

THE GEOGRAPHY OF POWER DID NOT CHANGE

Despite all these shifts the global hierarchy stayed almost the same. The three dominant markets, United States, United Kingdom and China, together they still account for the majority of global art sales.

THE ROLE OF “BEES”/ DIGITAL MARKETPLACES

In the report, “Bees” refers to online marketplaces connecting collectors, galleries, and dealers, not the insects. These platforms act as a bridge between traditional galleries and online audience, offering browsing, virtual viewings, and direct purchase. Last year 47% of dealers used online marketplaces to reach new collectors. These marketplaces helped smaller galleries gain visibility globally without high costs of international fairs. Bees are particularly important for the Millennial and Gen Z buyers, who increasingly discover artists and artworks online before visiting in person.

In short, online sales and digital marketplaces are growing steadily, but the have not replaced galleries, auctions, or art fairs.

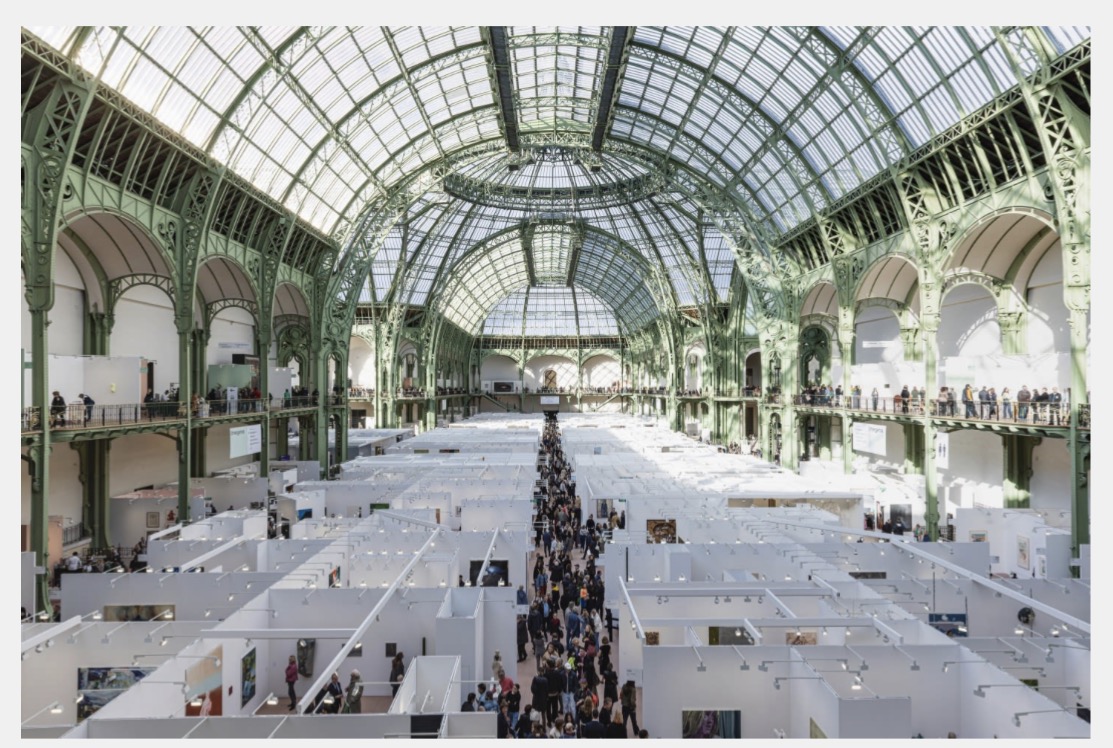

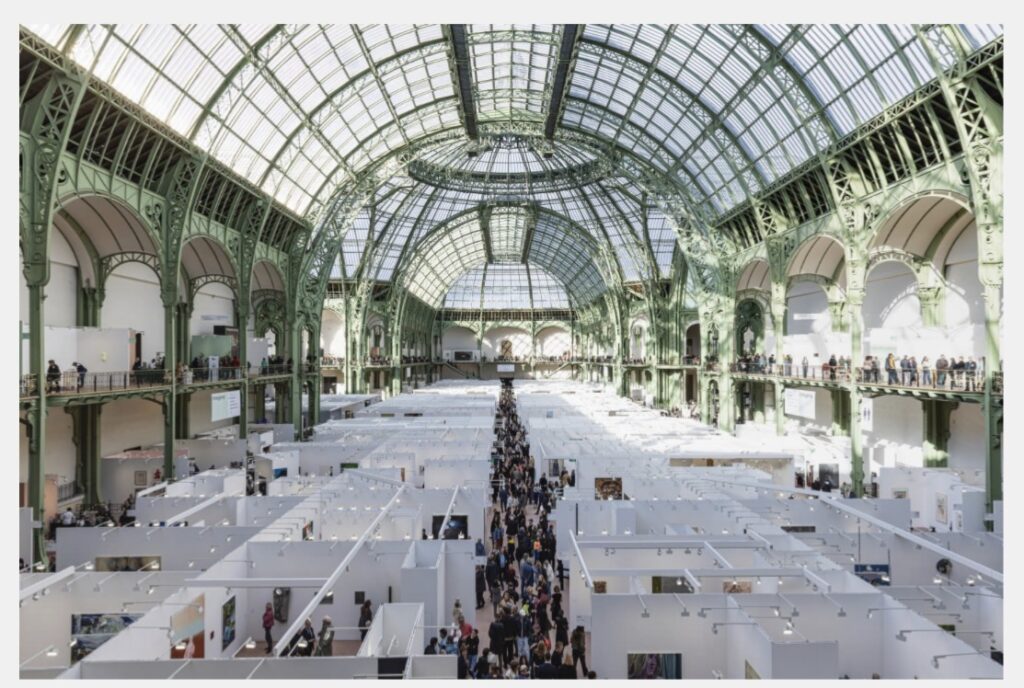

ART FAIRS: STILL ESSENCIAL, BUT MORE EXPENSIVE

In 2025 art fairs remained one of the most important engines of the art market, even more cautious economic climate. Important take away of the report around 31% of dealers say that art fairs remain one of the best places to meet new collectors.

According to the report, Art fairs are becoming increasingly expensive to participate in. Shipping, travel, and booth costs have risen sharply, making participation difficult for smaller galleries. Yet Art fairs remain the social and commercial center of the art market. They generate large share of sales and attract new collectors.

GALLERIES AND AUCTION HOUSES

For galleries, last year was difficult but not catastrophic. Overall sales by dealers fell about 6%, reaching around $34.1 billion. Smaller galleries were active, but large galleries struggled with big sales and higher costs.

Auction houses experienced and even sharper slowdown. Public auction sales fell significantly, especially for contemporary art and very expensive works.

The number of artworks selling for over 10 million dropped dramatically.

Shortly, big spectacular auctions slowed down, and more deals happened privately instead.

WOMEN COLLECTORS. GROWING FORCE

One of the most striking findings of the report is the growing influence of women collectors in the art market.

Women spent on average 46% more on art and antiques than men. 49% of the art works in women collections are by female artists, compared in men’s collections. Women collectors also appear more open to discovery: 55% frequently buy works by unknown artists compared with 44% of men.

Shortly, women collectors are not only spending more, but actively reshaping the market by supporting emerging artists and women artists.

GENERATION Z: THE NEW COLLECTORS

The report also shows a major generational shift in collecting. Millennials and Gen Z together now represent a large share of collectors, with Gen Z alone accounting for roughly 19% or art buyers.Again,gen Z alone representing around one- fifth of collectors. Their approach to collecting is notably different from that of older generations. Younger collectors devote a larger share of their wealth to art, are more willing to explore new media and digital works, and show a stronger commitment to diversity in the artists they acquire. In fact, according to the report, nearly 45 % of Gen Z spending goes to works by women artists, a significantly higher proportion than among older collectors.

My take away is , together women collectors and younger buyers are gradually reshaping the art market, making it more open, more diverse, and less dependent on the traditional hierarchy of trophy works.

WOMEN ARTISTS IN THE ART MARKET

One encouraging development highlighted in the report is the gradual but visible rise of women artists in the market, especially in the primary gallery sector. Works by women artists have also become more visible in museum acquisitions and institutional exhibitions, which often influenced the market demand. Although the overall share sales by women remains lower than men, the trajectory suggests a slow but meaningful shift. Collectors are beginning to recognize the historical gaps in the representation and are gradually correcting them through their purchases.

THE RETURN OR THE PHYSICAL ART WORLD

Another clear trend according to report is, collectors still prefer buying art in person.

Art fairs, gallery visit, and exhibitions remained the most important places to meet new buyers. The digital art market, which expanded during the pandemic, has stabilized but did not replace the physical experience of seeing art.

In other words, the art market confirmed something almost old fashioned: people still want to stand in front of the artwork before buying it.

THE REAL MEANING OF THE YEAR

If one idea summarizes the report, it is this; the art market is becoming less spectacular but more distributed. Instead of handful of monumental sales dominating the headlines, we are seeing; fewer ultra-expensive masterpieces, more mid-range collecting, more buyers entering the market, and specifically more art works circulating overall.

For art critics and observers, this may be taken as a healthy situation for the art market. When the market becomes slightly less obsessed with the record prices, it opens space for a wider range of artists and galleries to participate.